By the Members, of the Members & for the Members

By the Members, of the Members & for the Members

Significant development in additive manufacturing (AM) technologies commonly known as 3D printing has not only taken forward the automotive industry but have also improved ways in which products are designed and built. These improvements have increased scopes for lighter, cleaner and safer products; lower costs; and shorter lead time.

Latest developments in AM technologies, along with all the pertinent innovations in advanced materials, will benefit production within the automotive industry and also in other traditional manufacturing and supply chain pathways.

Summary

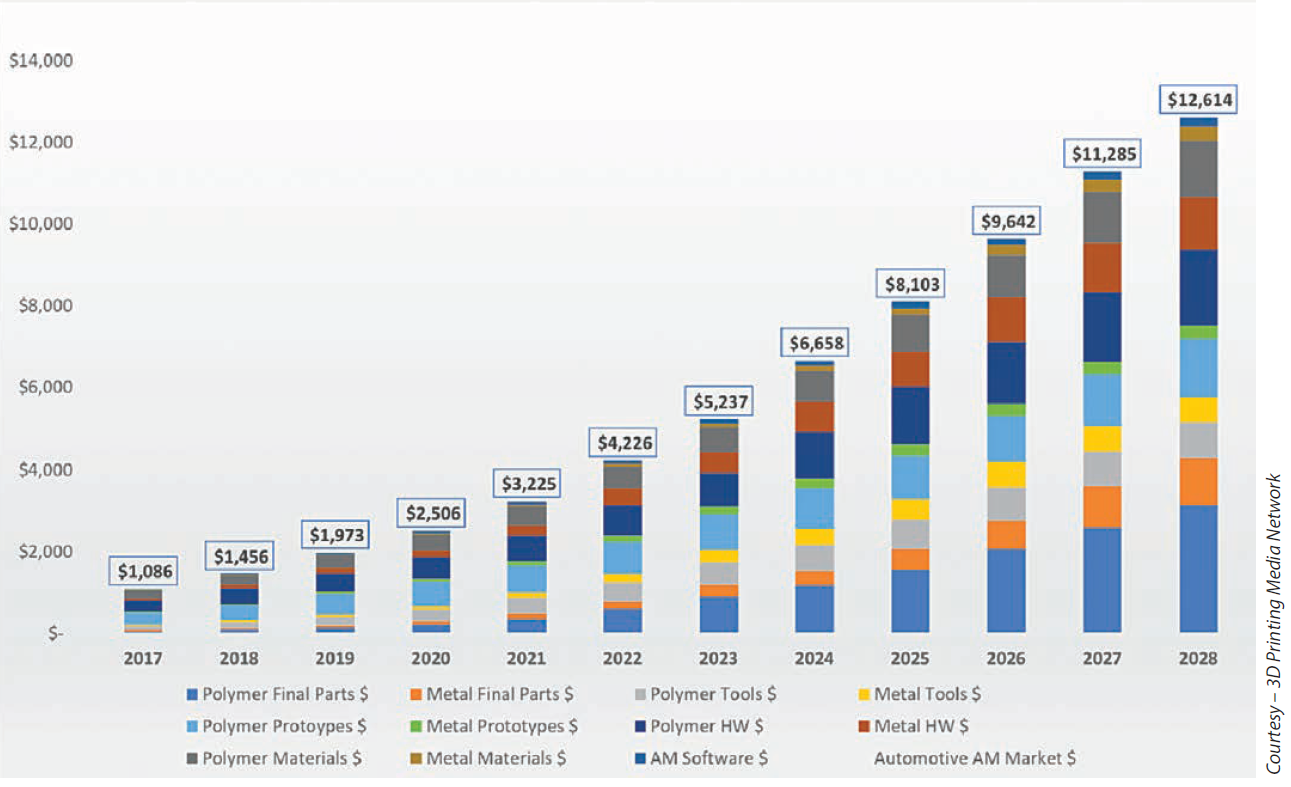

In the year 2016, a thorough analysis and forecast were released by SmarTech on automotive additive manufacturing. After two years, many new technologies have propelled the application of 3D printing technology into the future of the automotive industry. Automotive industrystakeholders are showing a greater interest in full industrialization and integration of the additive manufacturing process into their end-to-end production workflow beginning with software and passing through the actual hardware and ending services with an increased number of applications.

3D printing is in a much better position to develop its branches as primary manufacturing technology as prototyping and tooling thus creating a greater than ever opportunity for customized part production.

Driving Competitiveness – Role of AM

It was never easy to enter into the automotive industry especially at the top where the four largest OEMs had captured almost a third of the global industry which was $2 trillion in revenue in 2013. On the other hand, the parts and accessories industryis characterized by smaller players and is accounted for $1.5 trillion. To survive and succeed in such a competitive environment, innovation is the only key. We suppose there are two areas where AM will have the greatest influence on competition between automakers and potentially be a game changer:

1. Source of product novelty: AM can create components with fewer design limitations that often constrain more customary manufacturing processes. This suppleness is tremendously useful while manufacturing products with custom features, making it possible to addimproved functionalities such as integrated electrical wiring (through hollow structures), lesser weight (through lattice structure), and multifaceted geometries that are not possible through traditional processes.

2. Driver of supply chain revolution: By eliminating the need for new tooling and directly producing final parts, AM cuts down on overall lead time, thus getting better market responsiveness. In count, since AM generallyuses only the material that is required to produce a component, using it can radically reduce scrap and drive down material practice. Also AM manufactured lightweight components can lower handling costs, while on-demand andon-location production can lower inventory costs. Finally, AM can hold up decentralized production at low to medium scales.

Drivers and challenges in 3D printing’s espousal in the automotive industry

The accomplishment of AM’s future applications in the automotive domain depends mainly on how AM know-how evolves over the coming time. Wehave identified two drivers and four challenges that have the prospect to shape the future of additive manufacturing.

Driver 1: Large number of materials acquiescent to AMA wide variety of materials allows a greater number of properties to be entrenched into final products. Conventionally, AM applications have been constrained due to the limitations on the materialsthat can be used. While conventional manufacturing currently uses a wide variety of materials such as metals, alloys, and composites, AM has not been around long enough to see related developments.With a limited application of original materials in AM so far, these materials remain expensive.

However, a study has been steadily rolling to expand the assortment of obtainable materials. For instance, researchers at the University of Warwick have developed a low-cost amalgamated material thatcan be used particularly for additively manufacturing electronic components. In accumulation, the European FP7 Factories of the future development is researching methods to reduce construction costsof graphene-based thermoplastics for use in the construction of high-strength plastic mechanism.

Apart from fresh materials, new technologies that manufacture existing materials in a cost-effective manner also have a collision on the adoption of AM. Titanium, with its low density, high strength,and oxidization resistance, has strong demand in the automotive industry for its ability to create trivial, high-performance parts; yet widespread use is limited because the metal powder producedthrough current methods is expensive, costing about $200–400 per kilogram.

Driver 2: Improved AM-manufactured product quality and reduced post-processing

Parts produced through most AM technologies occasionally show variability due to thermal stress or the presence of voids. This results in lower repeatability, which is a challenge for high-volumeindustries such as automotive where quality and reliability are extremely important. One way to tackle this challenge is through machine qualification, where companies follow industry standards as wellas those of the AM technology providers.

Another concern in using AM is that the dimensional accurateness of final parts produced through AM is not always exactly on parity with those made through conventional manufacturing processes.Hybrid manufacturing guarantees a solution for addressing current unpredictability and finish quality concerns. Hybrid manufacturing refers to the mixture of AM with traditional techniquessuch as milling and forging. This transforms the perspective of a product from a “single unit to a series of characteristics” that can be produced through some combination of the techniques. One example of a hybrid manufacturing technique is ultrasonic additive manufacturing, a technology based on AM, using sound, that joins additive (ultrasonic welding) with subtractive (CNC milling)technologies to create metal parts. The application of AM allows these parts to have extraordinary features such as entrenched components, latticed or hollow structures, compound geometries, andmulti-material combinations, and the usage of CNC milling guarantees uniform finished quality.

Challenge 1: Finances of AM limited to low volume production

Productivity in the automotive industry is motivated by volume. In the year 2013, 86 million automobiles were manufactured globally. Given the huge volumes, the low production speed of AM is a significant impediment to its wider acceptance for direct part manufacturing. This has made high-speed AM a vital area of research. Recuperating build rates through the AM technology of SLM hasbeen an important focus in recent years, yet major breakthroughs have so far been hard to pin down.

Challenge 2: Manufacturing large parts

One of the major limitations of AM’s usefulness in the automotive industry is the limited build envelopes of existing technologies. Given this constraint, larger components such as body panels that are createdthrough AM still have to be attached together through processes such as welding or mechanical joining. To conquer this, low-cost AM technologies that can bear larger build sizes for metal parts have to be developed.There is already noteworthy research in progress. Oak Ridge National Laboratory and Lockheed Martin, has the potential to create components without any restrictions on size. Another way is the mammothstereolithography process developed by Materialise, which has a build wrapper of 2,100 mm x 680 mm x 800 mm—large enough to manufacture most of the large parts of an automobile. It was used to buildthe outer shell of the race car “Areion,” developed by Formula Group T, in just three weeks. However, since it can be applied only for building panels made of plastics, larger adoption has been slow.

Challenge 3: Talent scarcity

The exercise of any new technology requires people trained in skills precise to its manoeuvre; AM is no exception. AM-specific skills are indispensable in the areas of CAD design; AM machine making, operation,and maintenance; raw material preparation and management; analysis of finishing; and supply chain and project management. Currently, a significant bit of the necessary training is on the trade. With the expansion of AM applications, there will be a greater need for formal and extensive training and skill development programs in the submission and organization of AM. These programs requireconcerted action from academic institutions, AM service providers, and end-user industries to regulate training and create a stable and capable workforce.

Challenge 4: Rational property concerns

AM produce can’t be copyrighted but have to be patented on the basis of understandable demarcation. With a lack of clarity on what qualifies for patent protection and what does not, thereis a likelihood that counterfeit components will reproduce. According to the market research firm Gartner, the global automotive aftermarket parts subdomain, along with the toy, IT, and consumerproduct industries, could report as much as $15 billion in rational property larceny due to AM in 2016.

The road ahead

Despite the challenges, the truth remains that AM is a resourceful set of technologies that can support auto manufacturing companies in their pursuit of the strategic imperatives of performance, growth,and innovation. Considering the span of capabilities unlocked by AM, leaders of automotive companies should consider taking advantage of AM technologies to stay ahead of the competition.At present, automotive companies are using AM in the most conventional capacity, for swift prototyping. We do not currently see momentous product fruition or supply chain applications. However, automotivecompanies should consider exploring the other paths to obtain better value.

Tier 1 and 2 suppliers should look at exploiting AM potential along path II to serve consumers at locations closer to end users. Considering how auto consumers are becoming less willing to spend on replacementparts, players in the aftermarket segment can make maintenance and service cheaper by incorporating AM.

Developers in the auto industry should also closely scrutinize the Midtech and A&D industries that are setting the yardstick on how AM can be applied in support of large strategy. Driven by a domain needfor individualized products, Midtech began with mass customization. The automotive industry is a low-margin, revenue-intensive sector. To maintain productivity and market management, OEMs need to relook at their business model. Parts generalization and reduced assembly needs could have a direct blow on the supply base by dropping the size and intricacy of auto supply chains. As product novelty supported by AM increases, OEMs will locate that they have the chance to augment their business model by functioning a leaner supply chain.

While long-established manufacturing techniques are acutely entrenched and will keep on holding a governing position in the automotive industry, additive manufacturing is building inroads. Whilst AM will not become the only manufacturing technology in the outlook, it will, however, play a central role in determining the worldwide automotive landscape.

About Author:

Ankit Sahu CEO & Founder, ObjectifyTechnologies holds Bachelor of Engineering in Mechanical Engineering and Master of Science in Manufacturing Technology Engineering from Warwick University, UK. He founded Objectify Technologiesright after returning from UK in 2013, at SIIC IncubationCentre at IIT Kanpur. In just 6 years, the company has become one of the largest additive manufacturing solution providers in the country